Why Are Mlps Again and Again

An unprecedented combination of factors are meeting that we believe will brand midstream oil & gas MLPs an outperforming sector over coming years.

In today's richly-valued stock market, the MLP niche is total of bargains that offer safe and high yields to income-seeking investors. However, today the sector's historic undervaluation also offers investors interested in full return the prospect for equity-cost outperformance. Well selected, undervalued MLPs have the added benefit of lilliputian downside risk for long-term holders.

We believe the combination of these factors offer a rare opportunity for investors to secure attractive long-term full returns.

MLPs: Stuck In the Stock-Market place Doldrums

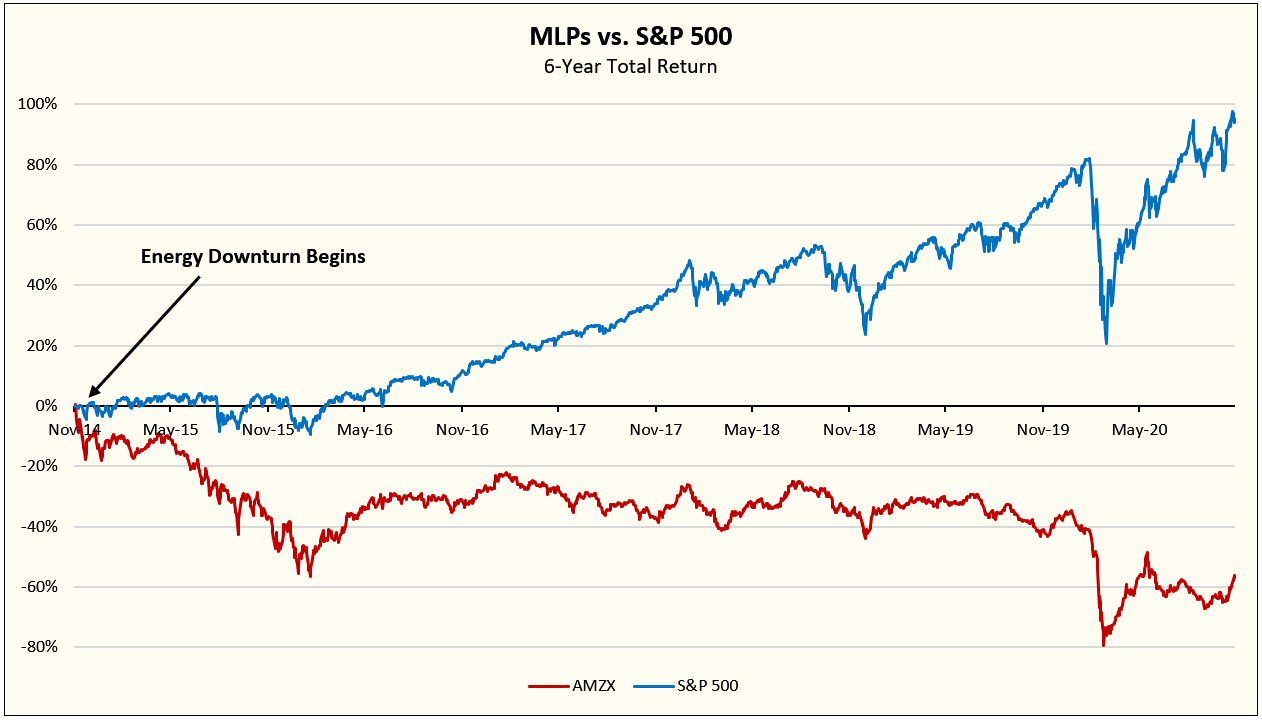

For years, MLPs have performed terribly, both in absolute terms and relative to the Due south&P 500. Deteriorating fundamentals, distribution cuts, and management mistreatment of unitholders have soured investors on the sector.

The sector's underperformance began with the onset of the energy-marketplace downturn in late 2014. The sector entered the downturn trading at height EV/EBITDA multiples—north of 15-times—and sporting an historically low distribution yield of less than half-dozen%. Equally oil and gas drillers reduced activity in response to collapsing oil prices, U.S. product volumes fell, and with them demand for midstream infrastructure. The resulting clasp on midstream margins inflicted massive harm upon the entire midstream manufacture.

So in late-2016, merely as midstream investors caught a glimpse of sunlight in the form of a dramatic rebound in U.South. oil and gas production, a spate of midstream project completions created excess chapters, thereby prolonging the sector's woes.

The deterioration in MLP fundamentals quarter afterward quarter reinforced investors' cynicism. As buyers grew deficient, trading-multiple pinch pressured MLP equities yr afterward twelvemonth, every bit tin can be seen in MLP relative performance beneath.

Many MLPs entered the downturn overleveraged and reliant on upper-case letter markets to fund capital spending. This led to a succession of more than 100 distribution cuts. As recurrent instances of mistreatment to unitholders from MLP management added insult to unitholder injury, information technology's no wonder why then many abandoned the sector.

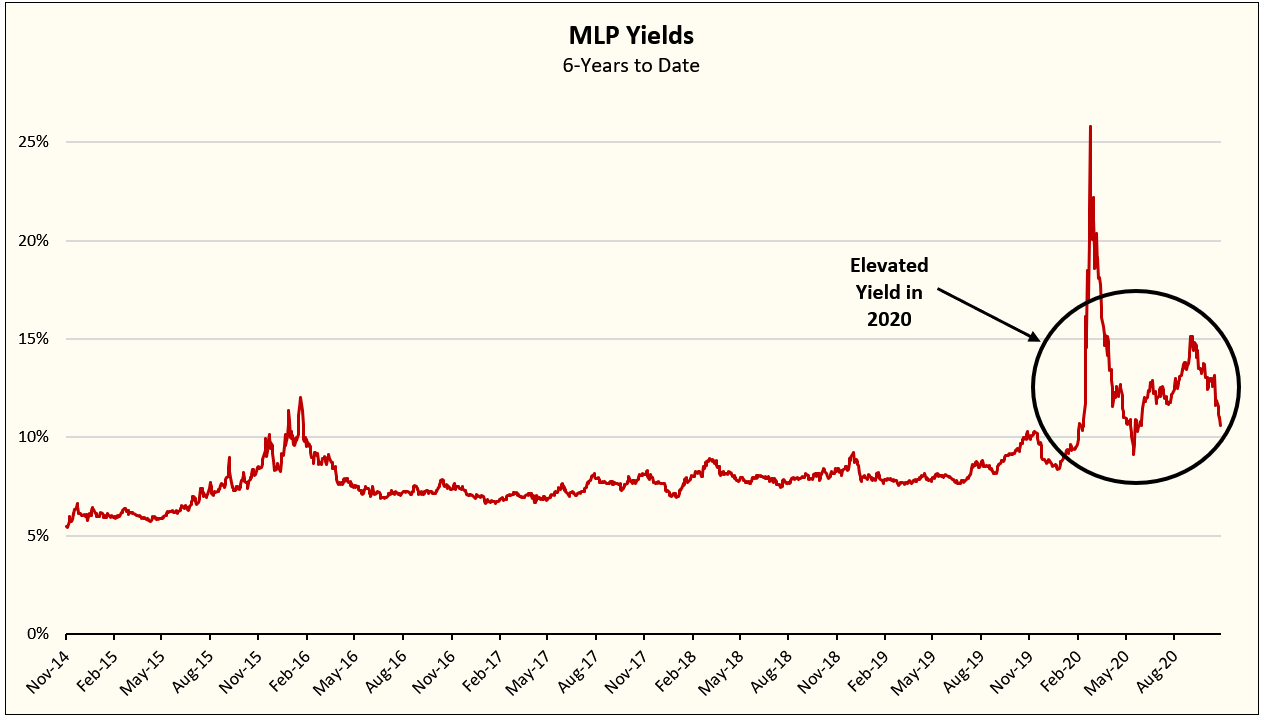

Rise Yields in a Yield-Starved World

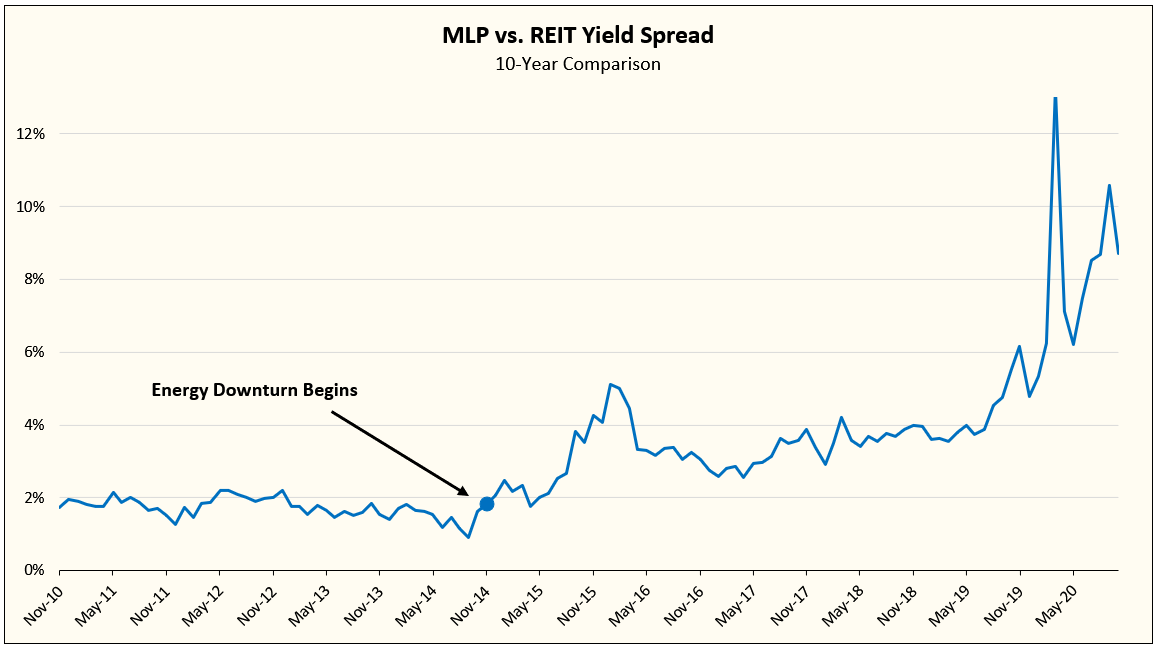

Falling unit of measurement prices take sent MLP yields to historic highs. Today'southward enormous yields are largely a effect of the MLP panic selling early this yr and bleak sentiment toward the sector ever since.

Equally shown in the chart below, MLP yields blew out in early on 2020 as unitholders sold in unison driven by both concerns over COVID-nineteen related demand devastation and the start of the oil price war past the Saudis.

This spike in MLP yields came in spite of 23 MLP distribution cuts and iv distribution suspensions in the first quarter alone.

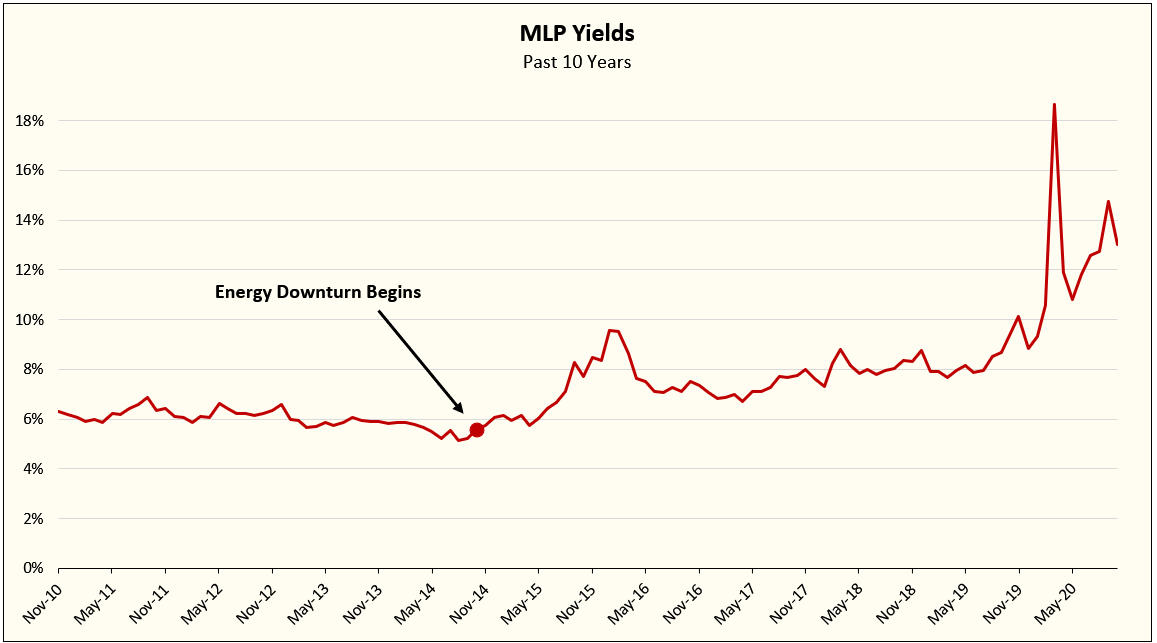

A 10-year chart puts the recent yield fasten in perspective relative to historical norms, both before the free energy market downturn and in the years thereafter.

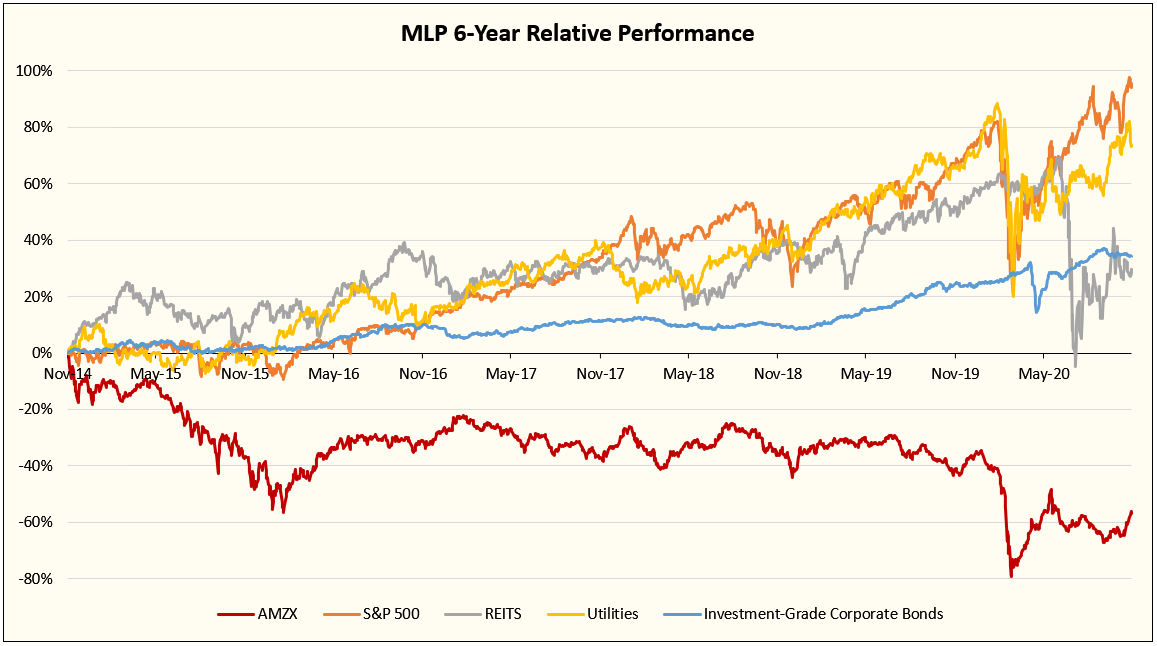

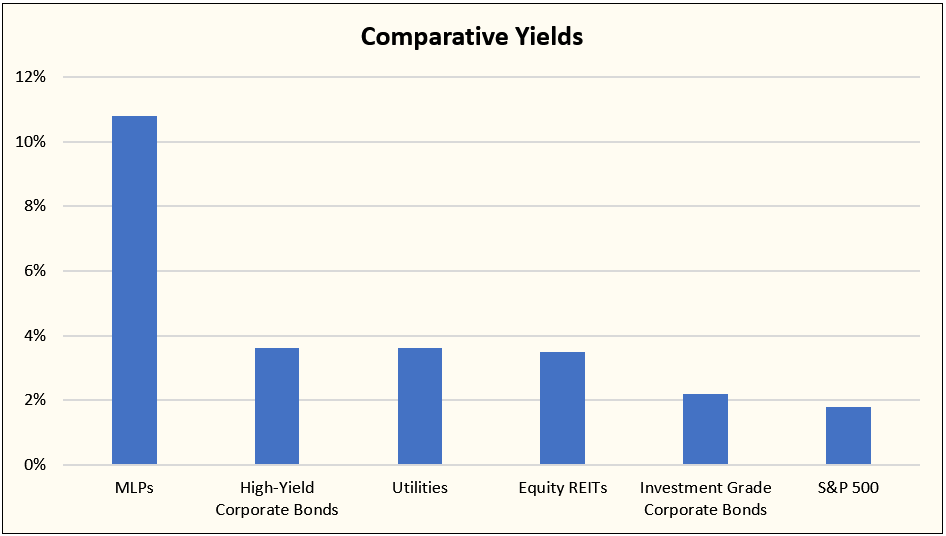

A comparing of MLP yields with other sectors sheds light on the MLP units' relative cheapness.

MLP units have dramatically underperformed all other nugget classes bought for yield. Consider, for instance, MLPs' underperformance versus utility stocks, equity REITs, and BBB corporate bonds, shown below.

And every bit their unit prices fell, relative yields soared. Today's MLP yields tower higher up the other loftier-yielding asset classes.

The spread betwixt MLPs and equity REITS is specially noteworthy, as it remains at historic highs.

MLP Fundamentals

An investor looking solely at MLP unit performance and yields will be surprised to acquire that MLP fundamentals accept held up surprisingly well in 2020 in the midst of unprecedented energy-industry turmoil in the wake of Covid-19.

In the second quarter, for example, when many MLP units' market prices were dropped by half in a matter of weeks, financial results for that quarter prove the sector's EBITDA holding up relatively well, with the pinnacle ten largest midstream MLPs posting a EBITDA turn down of 11% versus year-ago levels.

Then in the 3rd quarter, EBITDA bounced back more than strongly than expected, as shown in the following nautical chart.

Source: Goldman Sachs, November 2020.

Historically Cheap Disinterestedness + Improving Fundamentals = Opportunity

An investor has to wonder whether falling prices amid stable to improving fundamentals ways the 2020 MLP selloff has been overdone. Nosotros believe the answer is a resounding "YES," for the both the MLP sector at large likewise equally for select private names.

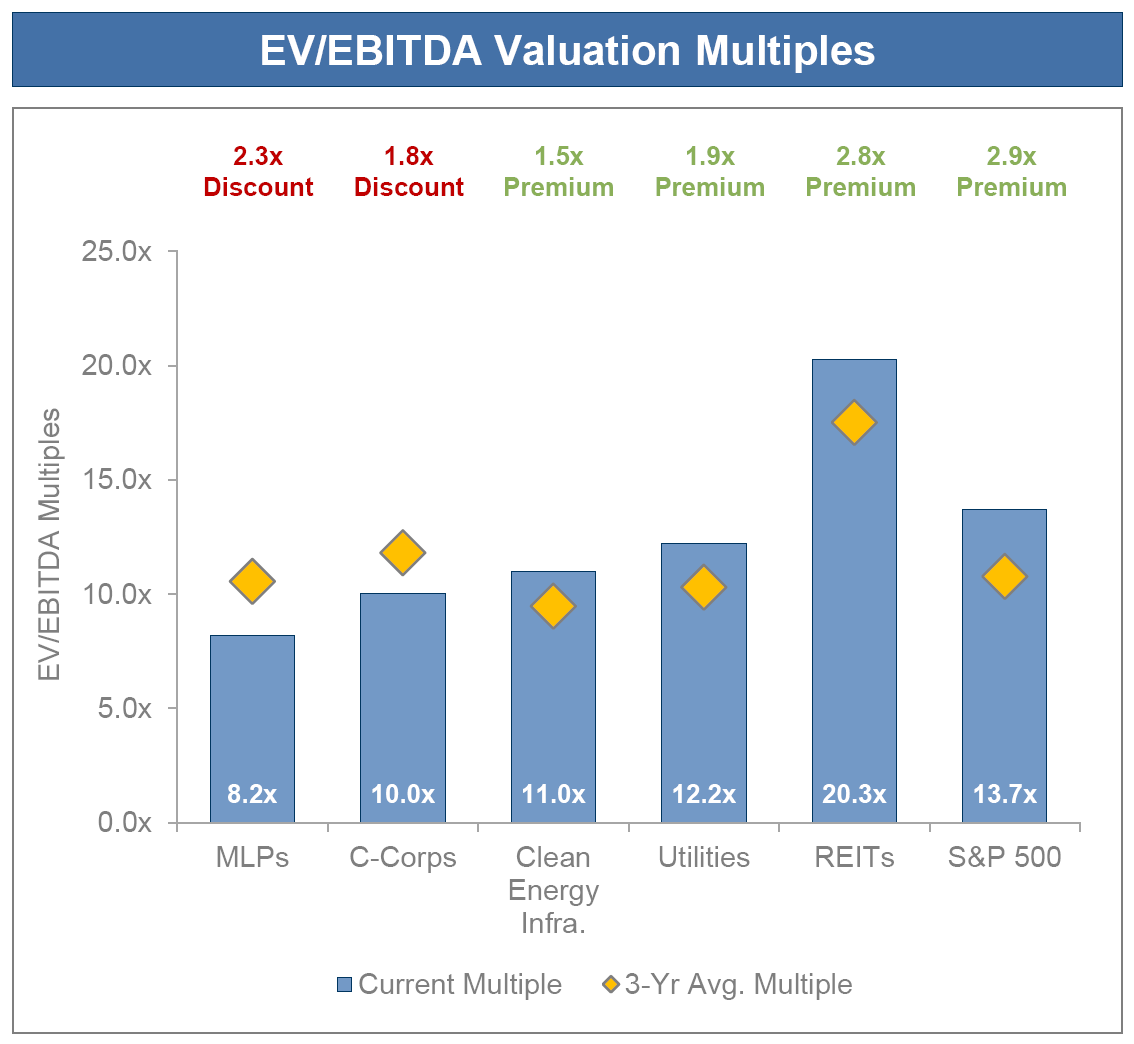

In fact, MLPs are undervalued based on nigh any key metric. For example, the group trades at an EV/EBITDA multiple of 8.2-times, well below its three-yr average of 10.v-times and its 10-year average of 11.6-times.

MLP EV/EBITDA multiples have fallen well beneath those of other higher-yielding sectors, as the chart below makes clear.

Source: Goldman Sachs, Nov. 2020.

Years of remainder-sheet repair and governance reform have lowered the industry's leverage and improved its operating metrics. Today's midstream MLP industry is characterized by healthier distribution coverage, growing free cash flow, and more than disciplined upper-case letter allocation.

As MLP EBITDA has rebounded from its second-quarter trough, while distribution cuts have alleviated financial pressure level, the sector'southward yield is well supported by greenbacks flow. The 10 largest MLPs, for example, showroom a healthy distribution-coverage ratio of one.7-times, which compares favorably with their coverage ratio of one.0 to ane.2-times before the downturn.

As improving energy-market place fundamentals support unit of measurement prices, any reversion toward historical norms will bring about impressive MLP outperformance. If the sector'southward current 10.8% yield were to revert back toward its historical average, unit values would increment anywhere from 35% to fourscore%.

Consider a comparison with disinterestedness REITs. MLP yields have soared relative to REIT yields, far out of proportion to the deterioration in MLP operating results, value harm, and business risk. If MLP yields reverted back to their celebrated norm of iv% in excess of REIT yields, assuming their distributions remain stable, MLP units would double from their electric current levels.

For the first time in years, MLP prospects announced far rosier than their beaten-upward equity prices imply. Today'south depressed MLP prices therefore offer a margin of safety between unit market price and economic value for a long-term holder, a rare combination in today's richly valued stock market.

High-Quality, Long-Lived Assets

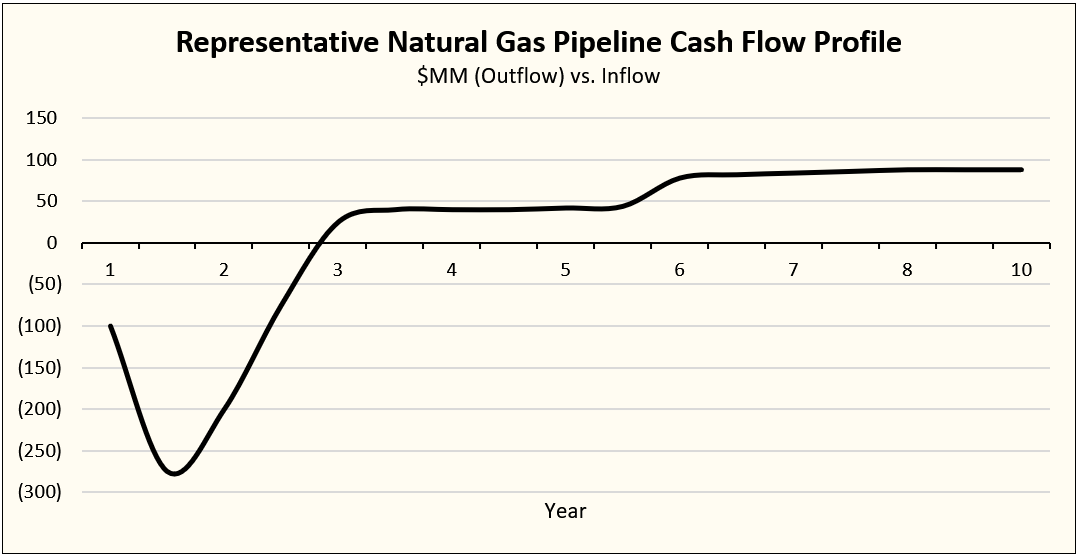

After all, the pipelines and other midstream infrastructure that MLPs ain are not inherently low-returning assets. When properly capitalized and prudently managed they can generate stable and attractive returns.

Midstream assets derive their render characteristics from their cash-catamenia profile. These avails consume large amounts of upper-case letter upfront during construction, but throw off significant greenbacks flow once placed in functioning. Moreover, they exhibit "toll road" economics that can generate reliable and stable cash menses over their multi-decade lives.

Even highly regulated midstream assets can earn a decent return, while provisions built into midstream service contracts hedge against inflation. Pipelines tend to appreciate in value when properly maintained, as population growth makes it difficult for potential new entrants to obtain rights of way. Activist pushback has too pushed up the toll of new pipelines, increasing the value of those already in operation.

An MLP direction team that is disciplined in choosing projects and adept at allocating uppercase can grow the MLPs economical value, and with it, the prospects for long-term upper-case letter appreciation.

Finding well-positioned and prudently-managed MLPs at bargain prices will be ane of our fundamental focus areas.

Catalysts

There are iii primary catalysts on the horizon that we believe volition bring most a re-rating of MLP equity trading multiples. As these catalysts materialize, they will crystallize the value proposition for owning MLP units.

Moreover, we believe they volition revitalize investor confidence in the sector, leading to capital inflows and sustained outperformance.

Catalyst #1: The Energy Market Recovery

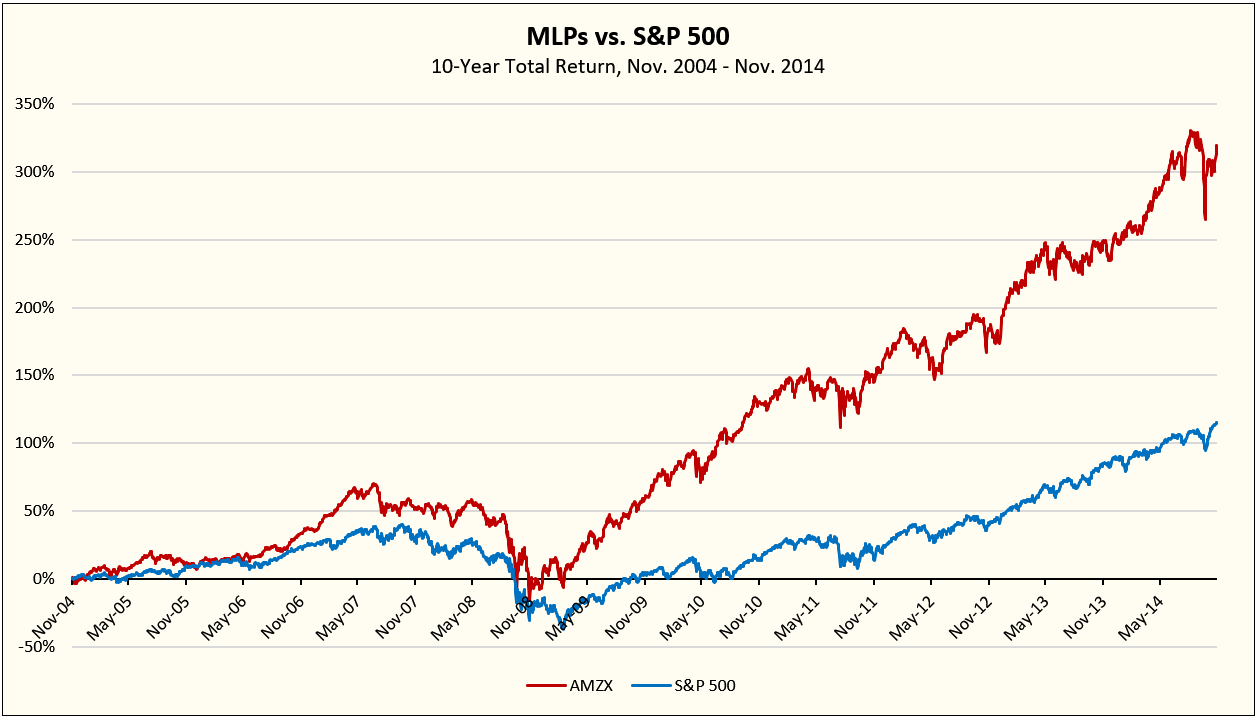

Information technology hasn't always been doom and gloom for the MLP sector. During the final energy industry upturn, MLPs outperformed mightily, as seen in the chart below, which illustrates the sector's x-yr relative performance against the S&P 500 showtime in 2004.

If the energy industry enters a new upturn (which we are currently forecasting), the concurrent improvements in fundamentals and investor sentiment volition accelerate MLP outperformance.

As covered extensively in our macro energy service, our view is that the past decade of underinvestment in global conventional oil supply, combined with restrained U.S. production growth, volition bring about a sustained ascension in oil prices every bit energy need recovers from its Covid-induced lows. College oil prices volition improve returns for projects across the manufacture, concenter capital to the energy industry, and increase the flow of bolt, the economic lifeblood of the midstream sector.

Nosotros believe the cyclical upturn in its infancy, and that MLPs are amidst the all-time positioned to benefit.

Goad #ii: Structural Governance Reform

MLPs accept been rife with conflicts of involvement between direction and unitholders. The management structure to which LP unitholders are subject field all but ensures that they end up on the losing side of any conflict. Still, recent industry reforms have aligned management and unitholder incentives more closely. It is important that electric current and prospective MLP investors sympathise what these reforms mean for MLP fundamentals and, eventually, investor attitudes toward the sector.

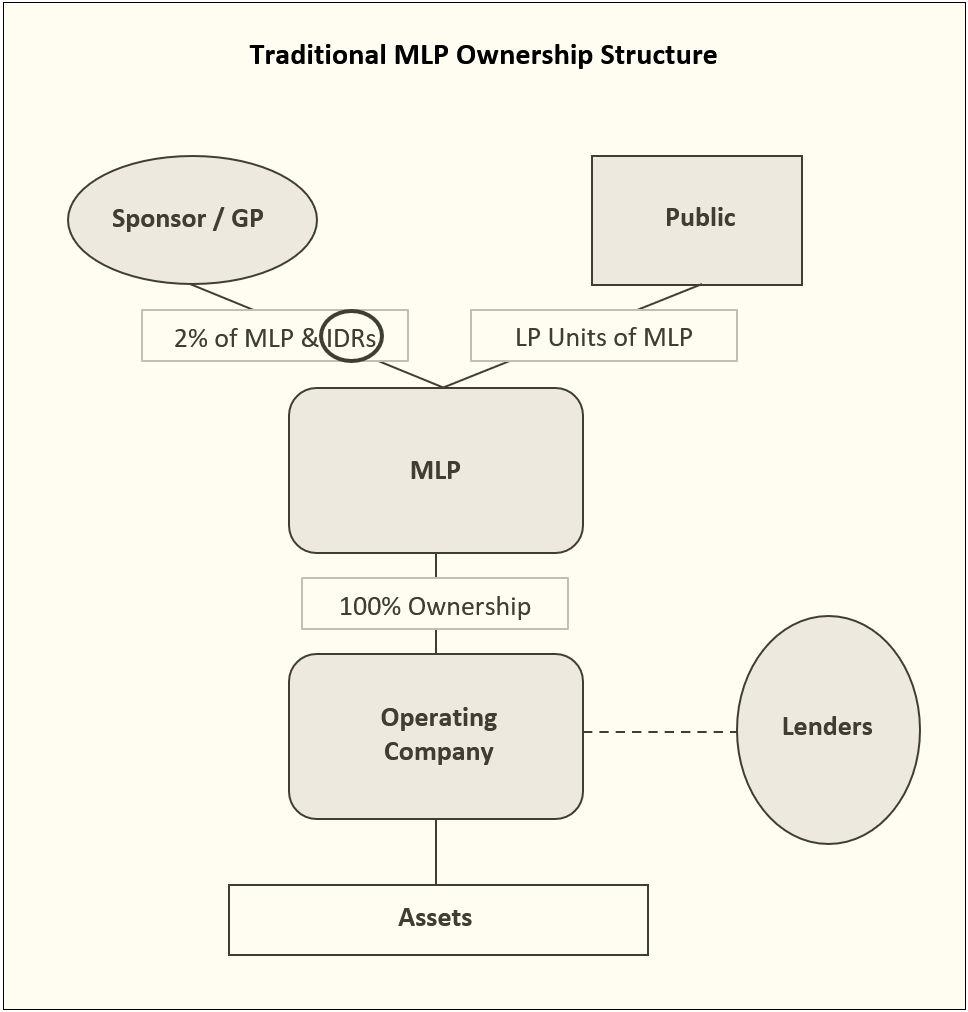

Traditionally, midstream MLPs are formed by a sponsor that sells its avails to the MLP. The sponsor forms a general partner entity (GP) to manage the business concern, and public limited partners (LPS) contribute capital to facilitate the MLP's buy of the sponsor's assets. The GP typically retains a small percent—around 2%—of the MLP.

The post-obit diagram depicts the standard MLP buying structure.

Many of the MLP governance problems revolve around "IDRs," or "incentive distribution rights," circled in blackness in the above diagram. Since MLPs are limited partnerships and not corporations, their management and boards of directors owe limited fiduciary duty to public LP unitholders. IDRs exploit this structural weakness in partnership governance.

IDRs are instruments endemic past the GP intended to incentivize management to grow the concern. To that cease, they apportion the GP a growing percentage of the incremental increment in MLP greenbacks distributions. Take, for example, an MLP that pays a quarterly distribution of $0.50 per unit at the time of its IPO. Initially, the GP will receive 2% of total distributions, commensurate with its 2% ownership involvement in the MLP. To "incentivize" management, the IDRs might stipulate that in one case distributions per LP unit rise to $0.55, the GP will be granted 15% of the increment in total distributions. So, once distributions per unit reach $0.65, the GP might receive 25% of the increase, and and then on until the GP is topped out at receiving 50% of the increase in distributions.

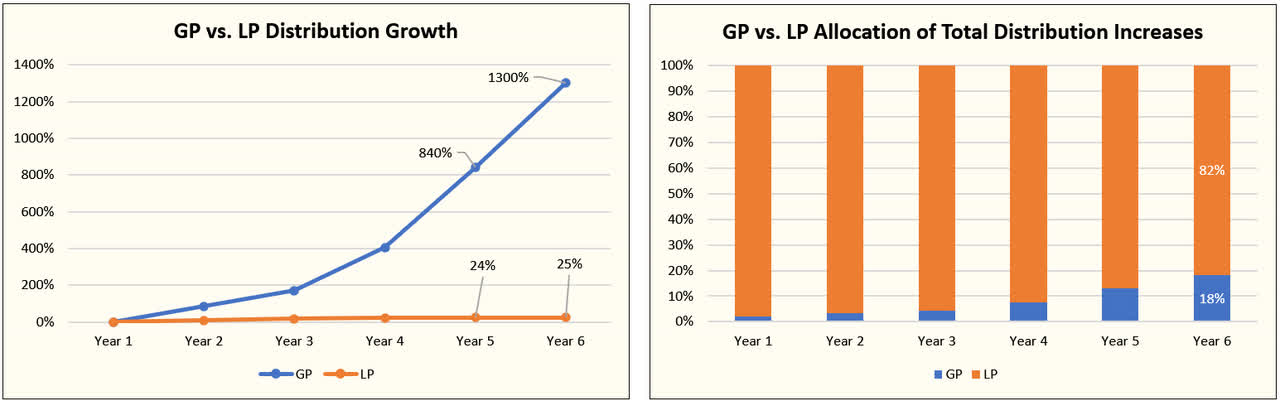

The post-obit charts draw the distribution growth charge per unit for the GP and LPs, equally well equally their respective share in the MLP's total distributions every bit they grow over time.

While IDRs have proven an effective means of increasing distributions, they have not always succeeded at ensuring long-term economic value creation for LPs. Past holding out the prospect of huge windfalls to management if distributions increase—regardless of performance for LPs—IDRs create an incentive structure wherein distribution growth is prioritized to a higher place all else, often at the expense of the LPs who own the overwhelming majority of capital at take a chance.

Consider, for instance, that an overarching focus on increasing distributions—as opposed to returns for LPs—may induce direction to accumulate cash-flowing assets regardless of their cost and/or complementary with the MLP'southward existing asset base. What's more, direction might fund these acquisitions by taking on too much debt. Perhaps after the conquering, management will increment the MLP'southward distributions to high levels that entail more than risk to LPs. Such undisciplined capital resource allotment would be detrimental to the LPs' long-term unit value. It would increase the likelihood that LPs neglect to earn a return above their toll of capital, while the GP earns multiples of the LPs' render.

MLP governance weaknesses have led to self-dealing amidst some GPs. Consider, for example, that there is zippo standing in the way of a GP issuing newly created LP units to the public for the purpose of purchasing inflated avails from the GP itself. Later on the GP has profited from the asset sale—which was effectuated by diluting existing LPs—information technology could then benefit further by boosting the MLP'south cash distributions, possibly thereby increasing the percentage of those distributions that flow into its own coffers, courtesy of its IDRs. In a self-dealing transactions like this, IDRs office every bit a thinly disguised mechanism for transferring wealth from LPs to the GP, whether rightly earned or not.

In our view, MLPs managed by GPs that ain substantial IDRs are uninvestable. The rewards offered past large and potentially growing LP distribution yields cannot outset the risks that arise from a structural conflict of interest between direction and unitholders. IDRs brand it probable that the deck volition always be stacked against unitholders, potentially to an egregious extent.

Fortunately for LPs, in contempo years many MLPs accept abandoned the utilize of IDRs. Since 2017, MLPs take had difficulty raising outside upper-case letter. To lower their cost of capital while making their equity and debt more palatable to new investors, many have undergone "simplification" transactions that eliminated their dual share structure and converted their IDRs to LP units. These transactions aligned management's economical interest more closely with public LP unitholders. They also ensured that boards of directors serve LP unitholders first and foremost, as opposed to being appreciative to the GP entity lone.

The new, LP-friendly model makes information technology more than probable that MLPs will:

- Lower their cost of capital

- Increment LP returns on capital

- Raise distributions in a prudent manner

- Increase distribution coverage ratios

- Fund growth through internally-generated cash menstruum

- Reduce equity issuance

- Resort to unit of measurement buybacks if unit prices go on to languish

- Pay downwardly debt

- Use debt they accept on more than judiciously

- Reduce unit of measurement market volatility

- Lower MLP yields every bit risks to LPs are reduced

Catalyst #3: Reduction in Growth Capital Expenditures

To conform surging U.S. oil and gas production, many midstream operators maxed out their balance sheets in order to boost growth capex. In doing so, nevertheless, they put their LP unitholders at adventure when revenues declined and admission to exterior capital letter grew deficient and expensive. With U.S. product slowing its growth over at lest the next few years, there volition be reduced demand for new midstream infrastructure, while existing infrastructure will see its capacity utilization grow. MLPs with few growth opportunities volition be able to harvest cash flows from the assets they built during the production boom, while remaining unburdened by obligations to fund boosted growth projects.

Consequently, many MLPs volition meet their cash flows increment while their growth uppercase spending requirements turn down. With relatively low maintenance needs, many MLPs stand up to generate big, and growing, amounts of organically-generated free cash flow.

Unlike REITs, which are required to distribute at to the lowest degree 90% of their income to shareholders in order to maintain their REIT status, MLPs face no such legal requirement. As MLP growth spending declines in coming quarters, MLPs will exist able to direct their excess cash menstruation toward paying downwardly debt, hiking unitholder distributions, buying back units, and/or funding new projects; all with organically generated cash.

Conclusion

All of the above puts MLPs squarely in the category of high-yielding assets with deeply undervalued market prices. HFIR Enquiry MLPs volition closely follow market developments and offer subscribers investment recommendations sourced from the sector'due south plentiful bargains.

Our coverage volition begin with some overarching themes of the MLP sector, which explain why MLPs accept gotten so cheap and why they are poised to outperform. Thereafter nosotros will profile two new investment ideas per week for subscribers. First and foremost, we volition seek safety in both equity values and payouts, but we will pursue opportunities that also feature capital appreciation, given the sector's dramatic undervaluation.

A guiding principle for long-term investing is that fundamentals affair. Equally today's favored sectors like technology continue to march higher, frequently without a fundamental rationale, their gamble for inflicting permanent loss grows. Investors seeking safety should instead plow to the pockets of undervaluation to minimize their adventure of loss and maximize their potential reward. Nosotros believe MLPs should be first on their listing. No sector features a more potent combination of favorable macro trends and sector-wide bargains, and nosotros look forward to riding what we believe will be a rising tide of MLP outperformance.

HFI Research'due south Dedicated MLP Service!

Piggybacking off of our successful main service, HFI Research, we are taking advantage of the current price disconnect in MLPs in relation to their fundamentals.

Our new service volition include:

- Subscribers to HFI Inquiry MLP will receive 4-6 exclusive idea write-ups per month.

- Existent-time portfolio tracking including what to buy, when the dividend will be paid, taxation implications, weighting, and much more.

As a launch special, we are giving everyone a two-week free trial along with a 20% discount! Come and meet for yourself what nosotros are all about!

Sign-upward here today!

Source: https://seekingalpha.com/article/4395067-why-investors-should-be-buying-mlps-hand-over-fist-today

0 Response to "Why Are Mlps Again and Again"

Post a Comment